To all you single guys out there, it’s not how you start the date, it’s how you finish it, sir. A lot of people can, you know, start the date with flowers and candy, but if you don’t finish the date – you know what I mean? — Shaquille O’Neal

Budget negotiations are kind of like an NBA game: there’s a lot of blah blah blah, get some nachos, some more blah blah blah, Jack Nicholson throws a fit, and then BAM! the real game (sometimes) commences in a flurry right at the end.

In the current tête-à-tête between Boehner and Obama regarding the resolution of the “fiscal cliff” (and, presumably, other related issues such as the AMT exemption extension, corporate taxes, and the debt ceiling), the public stances of the two sides have moved very little. Congressional Republicans (including Boehner) have accused Obama of slow walking “our economy right up to the ‘fiscal cliff.’” By this, I assume that Boehner means that Obama has not put forward an explicit proposal that, in theory, Congress could agree to and send to Obama for his signature.

Why has Obama not made an explicit offer? The answer to this is also the reason that budget negotiations are “like NBA games.” A fundamental point to recognize at the outset is what is called “selecting on the dependent variable”: when you analyze high-profile negotiations — negotiations where it makes any sense for one side to ask the other to make a public proposal — there is by presumption already “more at stake” than simply the policy implications of any ultimate agreement (or lack thereof).

In other words, the fact that we have a name for the “fiscal cliff” is proof that the choice of a path around (or over) the cliff carries more than simply fiscal repercussions. As I discussed before, there is some latent uncertainty about Boehner’s ability to deliver the votes of his GOP copartisans in the House. (There are similar concerns about Obama’s ability to deliver Democratic votes in the House but, leaving the Senate aside for the moment, this is necessarily at least somewhat ancillary to Boehner’s ability to deliver votes, since the GOP holds a majority of the seats.)

So, one strategic question that confronts Boehner is how to get GOP votes behind a deal to send to the Senate. But, before moving to that, consider the following point. If the deal is to involve any changes to the tax code (for example, partially or wholly extending the Bush tax cuts), the bill must originate in the House. In such a case, Boehner can’t wait for the Senate to “move first.” Given that public support for tax hikes on the wealthy is high, members of the Senate, regardless of their partisan affiliation, have no incentive to step forward with their own bill.

On the other hand, while he may not say it himself, many others have claimed that Obama “has a mandate” to raise taxes (and, depending on whom you ask, cut spending). One theory here is that the GOP might want to allow/require Obama to “own” the tax increase that would presumably be part of any public proposal he might make. I will will call this idea — that Congressional Republicans want to firmly affix “credit” for the tax increase/spending cuts to Obama — the albatross theory. However, this theory doesn’t do enough work, in my opinion, since Obama has already owned tax increases on the rich during the campaign. In addition, the theory I describe below, which I call the whack-a-mole theory, offers exactly an opposite prediction in terms of what (perhaps some of) the GOP would do if Obama offered a proposal.

Whack-A-Mole Politics. At the heart of the whack-a-mole theory is an adverse selection problem for the GOP. In this scenario, each member of the House is confronted with the problem of signaling his or her “true type” to his or her constituents. While some (or even all) members may want to resolve the fiscal cliff, each of them also arguably wants to send a signal to his or her constituents about the degree to which he or she would not compromise.

Think of it this way: a member from a somewhat conservative district wants to compromise, but also wants to demonstrate that he or she is also somewhat conservative. If he or she never has something to reject prior to agreeing to a resolution of the fiscal cliff, his or her constituents have no real reason to think that he or she isn’t a Democrat in Tea Party Clothing. Given that the Senate is not going to make a proposal, Obama must be the one to offer for the member to reject.

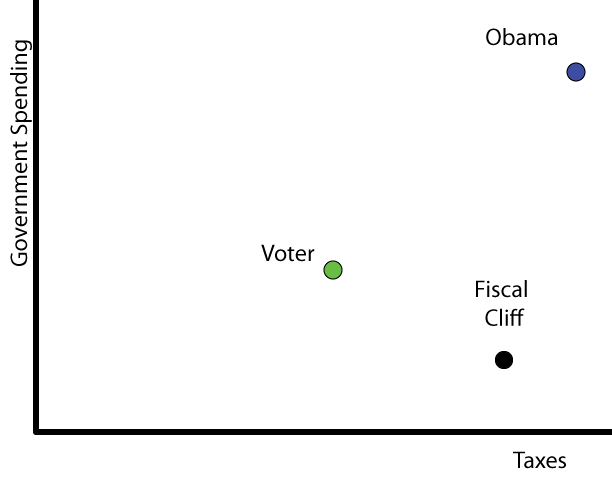

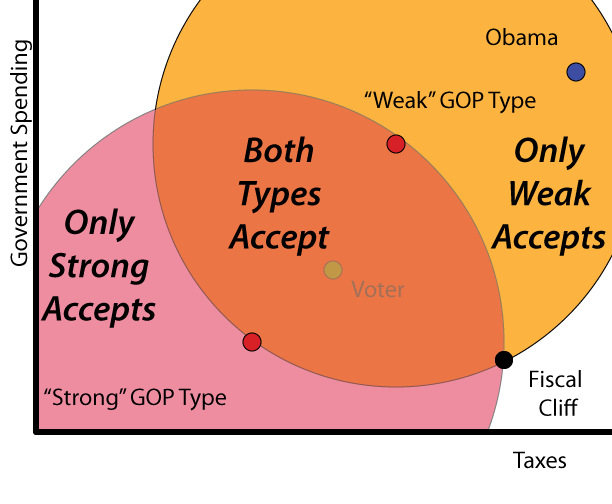

The strategic situation is captured (or, perhaps, butchered) in the graphic below. It portrays the political bargaining space as two dimensions: taxes and spending. For simplicity, I have located Obama’s “ideal policy” as “high taxes, high spending.” (This is all relative.) I have also located the hypothetical voter as “medium taxes, medium spending.” The fiscal cliff outcome is pictured as “high taxes, low spending.”

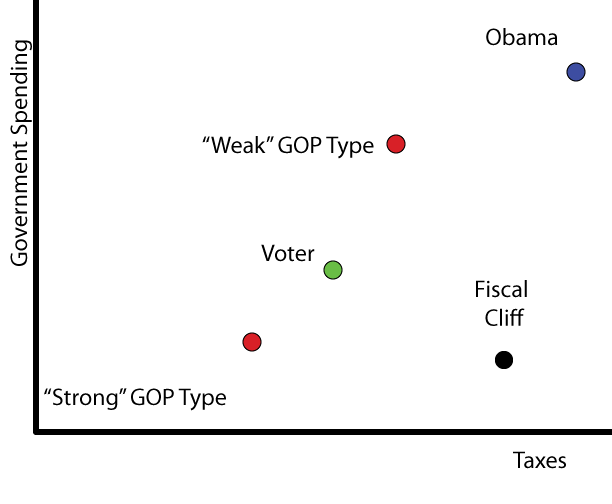

For simplicity, suppose that (the voter believes) there are two types of GOP incumbents: “Weak” and “Strong” Republicans. Weak Republicans like higher taxes and higher spending than Strong Republicans. This situation is portrayed in the next figure. The voter’s preferred levels of taxing and spending are closer to the Strong type (by design), so he or she would vote for a Strong Republican over a Weak Republican, ceteris paribus.

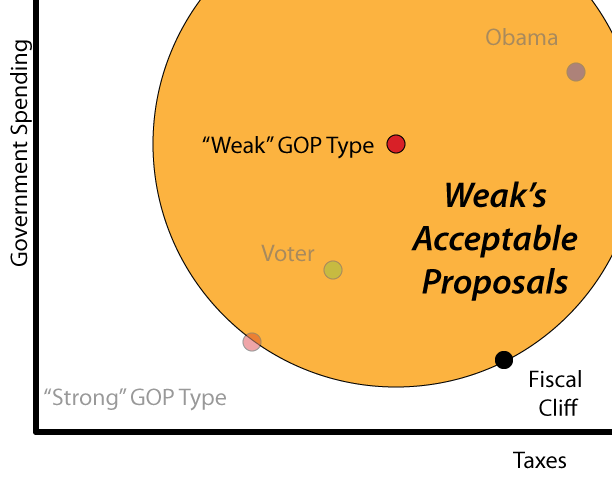

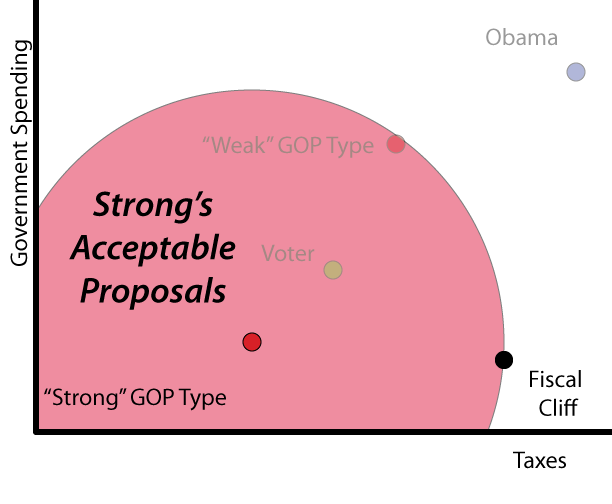

If presented with a take-it-or-leave-it proposal, (the voter thinks that) either type of incumbent would accept any proposal that is closer to the incumbent’s most-preferred combination of taxes and spending than the fiscal cliff. This set of proposals is pictured for each type in the next two figures.

Now, if we overlay these two figures, you find the sets of proposals that (the voter believes) would distinguish the Strong and Weak types of incumbents.

Okay, all well and good. Intuitively, Weak types accept proposals closer to Obama’s most-preferred combination than do Strong types. There are some proposals that both types would accept.

Now think about the fact that Obama does not, in fact, get to make a take-it-or-leave-it offer to the House. In fact, the reverse could be taken as a rough approximation of the situation. This suggests why the House GOP wants to make it seem like Obama should make a proposal — why he “has a mandate to raise taxes,” why this is the “time for him to lead.” To the degree voters think that rejecting an offer from Obama carries some risk of falling off the fiscal cliff (I won’t belabor the details of that here), both Strong and Weak types of incumbents in this example have an electoral reason to elicit a proposal from Obama. In particular, if Obama made a proposal, he would face two choices:

- Propose something that only weak types would accept, or

- Propose something that both types would accept.

(Proposing something that weak types would reject either results in policy really far from what Obama wants—so that he would then need to “pull a McConnell” and veto his own bill—or gets rejected with certainty by both types and doesn’t change the voter’s opinion about the GOP incumbent’s type.)

Presuming that electoral pressures on the incumbent are strong enough, choosing Option 1 leads to a rejection by both types and the GOP incumbent scoring “electoral points” with the voter regardless of the incumbent’s true type. (Note to my game theory-aware readers: no, this belief formation by the voter is generally inconsistent with the incumbent’s behavior. I must defer my discussion of voter’s beliefs until another time. Let’s just say that I am not sure how many voters regularly apply second-order logic to figure out that both types have an incentive to reject any proposal that only a weak incumbent would accept. Moving on…) In a political sense, then, Obama has an incentive to not propose and withhold the House GOP incumbents any chances to score points with their constituents by rejecting/attacking Obama’s proposal in an attempt to show that, yes, they will avert the fiscal cliff, but only along a conservative-enough path.

Option 2 is viable for Obama, but represents a distinct loss to Obama in terms of policy. That is, making such a proposal would provide Obama with a bill from the House that Obama would sign, but it is presumably worse (farther away from his preferred combination of taxes and spending) than he might be able to get if he forces the House to send something through the Senate first.

Please Let Me Refuse You… Before I Agree with You. The basic idea I want to get across here is that the GOP may have an incentive to get Obama to make a proposal because they want to reject it initially–directly the opposite of the “albatross” theory discussed above. The question of what Obama “should” do in this situation is more complicated, and requires a theory of the importance/role of time (and the Senate).

Speaking of time, I’m out of it right now. Maybe I’ll come back to the proposal problem in a later post. After all, like an NBA game, the real exciting stuff will probably occur at the end, as (in my opinion — and maybe the public’s) Obama doesn’t need to provide the GOP any opportunities to prove their bona fides. For now, I leave you with this.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}